How I Stopped Living Paycheck to Paycheck — Real Daily Money Wins

Remember that sinking feeling when your bank account hits zero before the month ends? I’ve been there — stressed, overspending, and clueless about where my money went. But after testing small daily changes, I finally took control. No magic tricks, just practical moves that actually work. This isn’t a get-rich-quick story — it’s about real financial shifts from someone who’s been in the trenches. Let me walk you through the exact moments that changed everything. These weren’t grand gestures or sudden windfalls. They were quiet, consistent decisions that slowly rebuilt my relationship with money. And if I could do it on an average income, so can you.

The Breaking Point: When My Wallet Finally Spoke Up

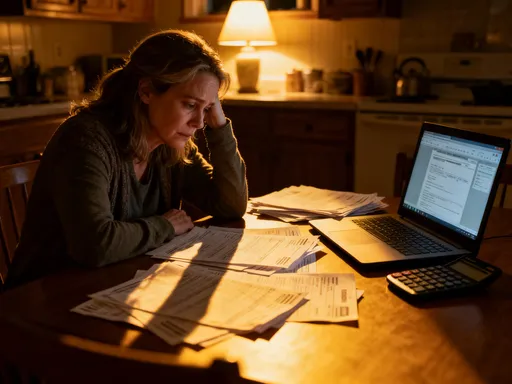

It happened at a grocery store, of all places. I was in the checkout line with a cart full of essentials — milk, bread, frozen vegetables, a few pantry items — nothing extravagant. I swiped my card, confident I had enough to cover it. The machine beeped. Declined. My face burned. I tried again. Same result. I had to remove items one by one until the total was low enough to go through. That moment wasn’t just about being short on cash — it was about realizing how disconnected I’d become from my own finances. I wasn’t living beyond my means in a dramatic way; I wasn’t dining out every night or buying luxury items. But the small leaks — the forgotten subscriptions, the daily lattes, the convenience meals — had quietly drained me dry.

That experience was the wake-up call I’d been avoiding for years. I had always told myself I’d get serious about money “next month” or “after the holidays.” But there was no next month that wouldn’t bring its own expenses. The truth was, I wasn’t waiting for the right time — I was waiting to feel ready. And I never would be if I kept ignoring the problem. The emotional toll was just as heavy as the financial one. I felt anxious every time I checked my balance. I avoided opening bills. I lied to myself about how much I’d spent. That grocery store incident stripped away the denial. I couldn’t pretend anymore. I needed a system, not just willpower. I needed to understand where my money was going, not just feel bad about it. And most importantly, I needed to stop treating money like an enemy and start seeing it as a tool — one I could learn to use with intention.

From that day forward, I committed to a single goal: awareness. I didn’t set a savings target or vow to cut out coffee forever. I simply promised myself I would stop flying blind. That decision — to pay attention — was the foundation of every change that followed. It wasn’t glamorous, but it was honest. And for the first time in years, I felt a flicker of control.

Tracking Every Dollar: The No-Judgment Money Diary

The first step I took was tracking every single expense — no exceptions, no shame. I downloaded a simple budgeting app that linked to my bank account and started reviewing my transactions daily. At first, it felt overwhelming. Seeing every dollar laid out in black and white was uncomfortable. There it was: $4.50 for coffee, $12.99 for a mobile game, $8.99 for a streaming service I hadn’t watched in months. The numbers didn’t lie. But instead of beating myself up, I made a rule: no judgment. This wasn’t about guilt. It was about data collection.

Over the next three weeks, patterns began to emerge. I noticed that my spending spiked on weekends, especially when I felt tired or lonely. I saw how often I used delivery apps after long workdays. I discovered three subscriptions I didn’t even remember signing up for — one was a free trial that had auto-renewed, another was a fitness app I used twice, and the third was a cloud storage plan I didn’t need. These weren’t major expenses on their own, but together, they added up to over $100 a month — money that could have gone toward savings or debt.

The real power of tracking wasn’t in cutting those expenses immediately — it was in understanding them. When you see a $5 latte every morning for a week, it stops being invisible. It becomes a choice. And once you see it, you can decide whether it’s worth it. I didn’t cancel everything at once. I let the data speak for itself. After a month of tracking, I sat down and reviewed my spending categories. I asked myself: What am I getting from this? Does this align with my values? Could I get the same benefit for less? This process wasn’t about deprivation. It was about alignment. And that shift in mindset — from avoidance to curiosity — made all the difference.

Tracking also helped me plan better. When I saw how much I typically spent on groceries, I could set a realistic weekly budget. When I noticed recurring medical co-pays, I started setting aside a small amount each month. The act of recording expenses transformed money from something abstract into something manageable. It gave me clarity. And clarity, I learned, is the first step toward control.

The 24-Hour Rule: How Waiting Changed My Spending

One of the most effective tools I adopted was the 24-hour rule: I would wait one full day before making any non-essential purchase. This simple pause created space between impulse and action. It didn’t mean I never bought the things I wanted — it meant I bought them with intention. The rule applied to anything that wasn’t a true necessity: clothes, gadgets, home decor, even books. If I saw something I liked, I’d add it to a wishlist or take a photo, then wait 24 hours before deciding.

The results were surprising. More than half the time, I lost interest. That trendy jacket I thought I needed? After a day, I realized I already had something similar. The kitchen gadget that promised to change my life? I remembered I barely used the one I already owned. But the most powerful moment came when I applied the rule to a $150 wireless speaker I’d been eyeing. I waited. And two days later, it went on sale for $99. Not only did I avoid an impulse buy, but I also saved over 30%. That felt like winning twice.

The psychology behind this rule is rooted in delayed gratification — the ability to resist short-term temptation for long-term gain. Our brains are wired to seek immediate rewards, which is why impulse spending feels so satisfying in the moment. But that satisfaction fades fast, often replaced by regret. The 24-hour rule interrupts that cycle. It gives your rational mind time to catch up with your emotional one. It allows you to ask: Do I really need this? Can I afford it without stress? Will I still want it tomorrow?

This practice also helped me redefine what “need” meant. I started distinguishing between convenience and necessity. Ordering dinner because I was too tired to cook felt like a need in the moment — but after 24 hours, I could see it as a choice I could prepare for. I began meal prepping on Sundays, so I had easy options during the week. The rule didn’t eliminate spending — it elevated it. I still bought things I loved, but now they felt earned, not impulsive. And that made them more enjoyable.

Paying Myself First — Without the Hype

“Pay yourself first” is a phrase you hear everywhere — but for years, I didn’t understand how to make it real. I thought it meant saving big money, and since I never had much left at the end of the month, I assumed it wasn’t for me. Then I realized my mistake: I was waiting to save what was left. But there was never anything left. The shift came when I started treating savings like a bill — non-negotiable and automatic.

I opened a separate online savings account and set up an automatic transfer of $25 from every paycheck. That was all I could afford at the time. No drama, no pressure. The key was consistency. Whether I transferred $25 or $5, I made sure something went in. Over time, that small amount grew. After six months, I had over $600 — more than I’d ever saved before. More importantly, I had built a habit.

I also started assigning purposes to my savings. Instead of one general account, I created mini-goals: $200 for car maintenance, $150 for medical co-pays, $100 for holiday gifts. This made saving feel more tangible. When I transferred money, I wasn’t just “saving” — I was preparing. I was protecting myself. That mental shift — from scarcity to preparation — changed how I viewed money. I wasn’t depriving myself; I was investing in my future stability.

Some months were tighter than others. There were times I was tempted to skip the transfer. But I reminded myself that the goal wasn’t perfection — it was progress. Even in tough months, I found ways to adjust: I’d save $10 instead of $25, or I’d use a small bonus to catch up. The account became a quiet source of pride. It wasn’t large by any measure, but it was mine. And it proved that even on a modest income, building a financial cushion was possible — one small transfer at a time.

Taming the Subscription Beast: What I Actually Canceled

Subscriptions are the silent budget killers. They start small — $5 here, $10 there — and before you know it, you’re paying over $100 a month for services you barely use. I decided to audit mine. I gathered all my bank statements from the past three months and listed every recurring charge. The total? $137.23. That was more than my electric bill. I was stunned.

I went through each one and asked: Do I use this? Do I enjoy it? Could I get the same value elsewhere? I kept my phone plan, internet, and one streaming service — the one I actually watched. I canceled two others I hadn’t touched in months. I downgraded my music app to the free tier, which was perfectly fine for my needs. I canceled a meal kit delivery I’d used twice and a cloud storage plan I didn’t understand. I also found a cheaper alternative for my budgeting app, switching from a monthly to an annual plan, which saved me $30 a year.

The emotional part was harder than I expected. Some subscriptions felt like part of my identity — like the fitness app that made me feel “healthy” even if I didn’t use it. Letting go felt like admitting failure. But I reframed it: I wasn’t failing. I was being honest. I was choosing to spend my money on things that truly mattered. The relief was immediate. The next month, my bank statement showed a $78 drop in recurring expenses. That wasn’t just money saved — it was mental space reclaimed. No more wondering where it went. No more guilt about unused services. Just clarity.

I also set a rule: no new subscription without a 24-hour wait and a written reason. This prevented mindless sign-ups. If I wanted to try something, I’d use the free trial — but I’d set a calendar reminder to cancel before it renewed. That simple step saved me from dozens of accidental charges. Taming the subscription beast wasn’t about cutting everything — it was about curating. I kept what added real value and let go of the rest. And that monthly breathing room made a bigger difference than I ever expected.

Grocery Wins: How My Cart Became a Budget Superpower

Groceries were my second-largest expense after rent. I used to shop without a plan, grabbing whatever looked convenient. That changed when I started meal planning. Every Sunday, I’d check what I already had, review the weekly sales at my local store, and plan five dinners and a few lunches. I’d write a list and stick to it. No deviations. This alone cut my grocery bill by nearly 30%.

I also started using the cash envelope method for food. I’d withdraw $120 every week and put it in an envelope labeled “Groceries.” Once the cash was gone, that was it. No more spending until the next week. This created a hard boundary that my card never did. Seeing the physical money shrink made me more mindful. I started comparing prices, choosing store brands, and buying in bulk when it made sense. I learned to cook in batches — making large portions of soup, chili, or roasted vegetables that I could eat throughout the week. This saved time, reduced stress, and cut down on takeout.

One of my biggest wins was learning to embrace “imperfect” produce. I’d buy fruits and vegetables that were slightly bruised or nearing their expiration date — they were often 50% off and still perfectly good. I’d use them in smoothies, soups, or baked dishes. This not only saved money but also reduced food waste. I also started shopping later in the day, when stores often mark down perishable items. A $6 container of chicken might be $3 by 7 p.m. — and I’d use it in a stir-fry or salad.

Meal planning didn’t eliminate spontaneity — it made room for it. Because I had most meals covered, I could treat myself to a nice dinner out once a month without guilt. I wasn’t depriving myself; I was prioritizing. My grocery cart became a symbol of control. It wasn’t full of impulse buys — it was full of intention. And that shift made all the difference.

Building a Mini Emergency Fund: My $500 Safety Net

For years, any unexpected expense — a flat tire, a doctor’s visit, a broken appliance — sent me into panic mode. I’d have to use a credit card or borrow from a friend. That cycle of stress and debt was exhausting. I knew I needed an emergency fund, but the idea of saving $1,000 or more felt impossible. So I started small: my goal was $500. Just five hundred dollars to cover minor surprises without derailing everything.

I built it slowly. I saved my tax refund — $220 — and put it straight into a high-yield savings account. I rounded up every purchase and transferred the difference automatically. A $3.80 coffee became a $0.20 deposit. Over time, those cents added up. I also saved small windfalls: birthday money, a work bonus, even a $20 I found in an old coat pocket. I treated every extra dollar as a chance to strengthen my safety net.

When my car battery died six months later, I had $512 in my emergency fund. I paid the $180 repair without hesitation. No stress. No debt. No late fees. That moment was transformative. It wasn’t just about fixing a car — it was about proving to myself that I could handle life’s little curveballs. The $500 didn’t solve every problem, but it prevented a small issue from becoming a financial crisis.

The psychological benefit was even greater than the financial one. I felt calmer. More confident. I wasn’t living in constant fear of the next unexpected bill. That sense of security made it easier to stick to my budget, to keep saving, to make thoughtful choices. The mini emergency fund wasn’t a finish line — it was a foundation. And from there, I started planning for the next level: $1,000, then three months of expenses. But it all began with that first $500 — a small number with a big impact.

Small Steps, Real Control

Looking back, I didn’t change my life overnight. There was no single decision that fixed everything. It was the accumulation of small, consistent actions — tracking a receipt, waiting a day, transferring $25, canceling one subscription, sticking to a list. These weren’t dramatic moves, but they were powerful because they were sustainable. Financial freedom isn’t about perfection. It’s about progress. It’s about showing up for yourself, day after day, with honesty and care.

What I’ve learned is that money isn’t just about numbers — it’s about behavior, mindset, and self-trust. When you start making intentional choices, even small ones, you build confidence. That confidence leads to bigger changes. You stop feeling like a victim of your circumstances and start feeling like the author of your life. You realize you don’t need a raise to feel secure — you need a system.

If you’re tired of living paycheck to paycheck, know this: you don’t have to do everything at once. Start with one thing. Track your spending for a week. Try the 24-hour rule. Cancel one subscription. Save $10. These tiny wins add up. They create momentum. And momentum creates change. You don’t have to be perfect. You just have to begin. Because the truth is, financial control isn’t reserved for the wealthy or the disciplined. It’s available to anyone willing to take the first step — and the next, and the next. And that includes you.